Historically, physical ledgers have been used to keep a record of people’s assets and their transactions with money. Learn more about how we got from there to blockchain – a decentralised distributed digital ledger technology that has taken the world by storm!

A Simplified Introduction to Blockchain

Are you someone who knows absolutely nothing about blockchain? Or perhaps you have heard of the term, maybe even have some grasp of the blockchain technology, but still struggle to wrap your head around it?

Whichever group you belong to, read on! You will definitely benefit from this beginner-friendly and simplified introduction to blockchain. It will provide all the context you need to understand how we got from physical ledgers all the way to this amazing technology!

The outline of this article is as follows:

- The early days of blockchain

- How things were done before blockchain

- Blockchain as a distributed digital ledger

- Is blockchain only used for Bitcoin?

- Conclusion

The early days of blockchain

Let’s start from the beginning. Blockchain is a relatively new technology, a bit more than a decade old. It has its origins in a white paper published in late 2008 by Satoshi Nakamoto, called “Bitcoin: A Peer-to-Peer Electronic Cash System”. Yes, the title says Bitcoin, not Blockchain. The word blockchain, in the way we use it now as a single word, does not even appear in this original paper.

But this paper has definitely laid the groundworks on blockchain, even if that name was not coined back in 2008 yet. This is so because the underlying technology of Bitcoin described in the paper is what we essentially refer to as the blockchain today. Even though the word blockchain does not appear in the paper as a single word, the words block and chain do appear everywhere in it. We’ve covered what those terms mean exactly and how blockchain works in this article on the internals of blockchain.

Even though Bitcoin and blockchain have a certain dependency and correlation between them, blockchain is definitely not all about Bitcoin.

Let’s repeat this, as it’s very important.

Blockchain is not just about Bitcoin.

In fact, blockchain is not even only about cryptocurrency, it’s not only for finance. Nowadays, most businesses interested in blockchain are using it for reasons that have nothing to do with Bitcoin or any other cryptocurrency. More on this later in the article.

But now, in order to understand the true value that blockchain brings, it’s helpful to go back in time for a moment. Let’s forget about blockchain, and even about computers for a short while. And let’s talk instead about how people have done things hundreds of years ago.

How things were done before blockchain

For hundreds of years people have used ledgers, big heavy books to keep track of accounts and transactions. Here’s how old ledgers might have looked in the past (though they didn’t have to be dusty and old to serve their purpose).

In fact, even today anyone can go to an office supply store and buy a paper ledger which could serve the same purpose of creating a permanent record of a person’s account or transactions. But we should say, quote unquote “permanent”, because such a record on a physical ledger would easily be damaged. The ledger could be lost, torn, or its quality lost due to any environmental or external factor.

But there are even more issues associated with them. The ledgers could be filled out incorrectly. Someone could write an entry in the wrong place, or miscalculate a balance, or forget to write an entry at all. These could happen unintentionally, but there could be malicious deception as well. Someone might even change an old transaction after it was recorded in the ledger.

Anyway, let’s get back to how these ledgers were traditionally used. To track an account, you’d begin with writing down the account and its initial balance to the ledger. Whatever happens next, you never go back and change that first entry. Rather, you just keep adding new entries to the ledger for every change on that account, for every new debit or new credit. This way, the ledger keeps track of the full history.

So you’d use this big book to track everything, all the transactions along with the details of each, like the date when the transaction happened, the amount transacted, the parties involved.

These transactions could be just about anything, from something trivial like the purchase of a spoon, to something like the buying of an acre of land, a house or a building. Ledgers could also be used to record the details of loans and money owed. It could be a continual record of who owns certain assets, or how they are being lent from one party to the other.

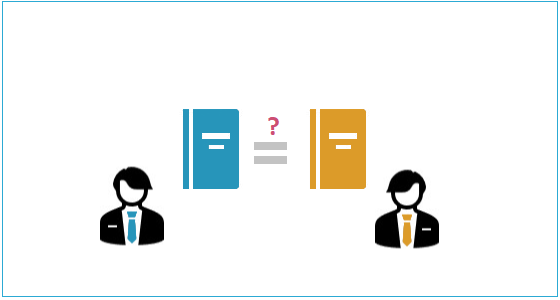

However, transaction details weren’t just recorded in a single ledger, but in multiple ones. If one entity decided to buy a chair from another entity, that’s something the first entity would record in their ledger as an expense. It’s an expense for them because they spent money on the chair. On the other hand, the second entity (the seller) would record the same transaction in their ledger as a profit, because they earned money. Same transaction, different point of views, so to say.

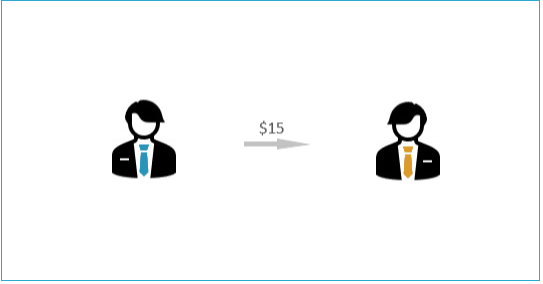

And herein lies perhaps the biggest problem of traditional ledgers. If we’re dealing with transactions recorded in different ledgers and involving different parties, the ledgers can be inconsistent and disagree about the same events. So if Joe borrowed $15 from Jack, Joe could say: “I paid you back the money, look at my ledger”. But Jack might be quick to reply: “Nope, no such payment record in my ledger, you still owe me”.

So what do we do in this case? Whose ledger should we trust, Jack’s or Joe’s? How do we make that decision?

Any discrepancy can be a real problem if there is no agreed way on how to settle it.

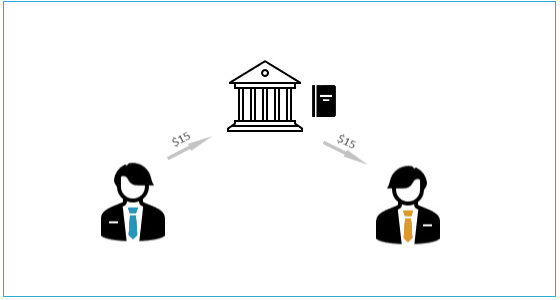

Introducing intermediaries

And this is how third parties have historically become involved as intermediaries in these kinds of situations. With third parties involved, transactions no longer flow directly between the buyer and the seller. All money flows through this third party. Hence, we trust the ledger of this third party, instead of having to decide between the ledgers of the buyer or the seller. The third party’s ledger is the authoritative one, the single source of truth.

Nowadays, having third parties involved in all our transactions is the norm. It is part of our daily lives. It is so common that we don’t even notice it for the most part. Almost every transaction and money exchange happens through an intermediary today.

When you apply your card to a POS terminal in a local shop, it might feel as if you are paying directly to the shop owner for the goods or services received. But remember that banks, credit card companies and maybe even other intermediaries are involved behind that card. You are not giving your money directly to the shop owner. Instead, your money is flowing from the account in your bank, through the credit card company, to the shop owner’s bank and finally, to his account there.

All these intermediary institutions add a cost to the transaction and often a delay to it as well. Also, these intermediaries now have information on how you spend your money. At first, their knowledge that you are buying groceries from a local shop might not seem such a big deal. But remember that this means they also have a way to track your spending habits, and hence the locations you visit as well. So there is also a privacy issue involved here.

Let’s get back to our main discussion on the need for these third parties. We need them (i.e., their ledger) to act as the single authoritative source of truth, in order to avoid disagreement and fraud between the parties involved in the transaction. Without the ledger of this authoritative institution, we wouldn’t know how to decide which party to trust. We can’t just decide to trust the version of the events and facts as written in the ledger of one party involved, as opposed to the ledger of the other party. Especially not when they disagree.

So just imagine:

What if there was only one ledger?

Let’s revisit the “Joe borrowed $15 from Jack” scenario, in the light of a single ledger. Let’s assume this single ledger exists, and that whatever Joe writes about this transaction, it “magically” appears for Jack as well. So if either Joe or Jack write a new transaction, it magically appears in this single ledger. And even more, once that transaction appears, it’s not changeable. Neither of the two, nor anyone else for that matter, can delete it or alter it.

So what could we do if this magical single ledger did actually exist? What could we do if a shared, incorruptible, secure, and authoritative ledger existed indeed? A ledger that could become a reliable source of truth, because it also contained historical data? One that could serve as proof that yes, Sarah really does own the entity she says she owns, and yes, Mike does own the entity or asset he says he owns. And that yes, Joe did borrow $15 from Jack.

Well then, if the above would be a reality and this incorruptible, secure and trustworthy ledger would exist, then we wouldn’t need any intermediary institution. By removing the intermediaries, transactions would become cheaper and faster. A lot of transactions of any type or size could be performed faster without their previous inherent costs. It would also benefit privacy, as the intermediaries would no longer be able to track so much data around how people spend their money

And this magical ledger wouldn’t have to serve just two people. It would rather be possible to share it between three or 300 or 3000 people. Even more, it could be completely public. And the best part of it is, we wouldn’t have to trust every single party involved. We wouldn’t have to like them or know them, as long as we can all trust the ledger and agree it to be the authority, the source of truth.

Blockchain as a distributed digital ledger

And as you might have guessed already, the world has been super excited for the past decade or so, that the technology that would enable a shared, secure and trustworthy digital ledger is actually here. It is known as the blockchain.

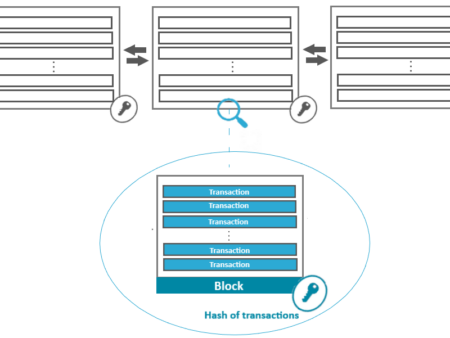

You might have also heard the term distributed ledger or shared ledger used for the blockchain. This is because the whole point of this technology is to create a distributed digital ledger, in the form of a network where information is replicated across many different computers. So when any participant in this network adds a new record, this record is automatically added (replicated) across all the different computers in the network. These computers are also known as network nodes.

The defining characteristic that makes blockchain very different from a traditional distributed database, is that this distributed ledger is not owned by a single person. Neither it is owned by any organisation or institution or government. There is no single administrator, no one in charge, because the data is not just on a particular computer in a server room in a company. It is decentralised.

So addition of new entries to the blockchain isn’t performed in one master node. There is no master node. Blockchain is a complete peer-to-peer network, and new transactions can be added at any time by any node. Then the newly added transactions would be swiftly and automatically replicated to all the other nodes in the network. Blockchain’s ability to act as a single source of truth works incredibly well in the financial industry, but it’s also immensely useful for a lot more.

Is Blockchain only used for Bitcoin?

Let’s revisit this important question again – is blockchain only used for Bitcoin?

The answer is a definite NO. But because blockchain was originally developed to support Bitcoin, this historical association between blockchain and cryptocurrencies has led to several misunderstandings. Many people mistakingly think of blockchain as something applicable to Bitcoin or online financial services only.

This has actually happened with other inventions in the past. A concept might have been invented to fix one specific problem or meet one specific need, and then people figured out it could be applied to solve a whole bunch of different problems.

Consider this example from the past. A technology we now use very differently from the way it was first intended is the World Wide Web. The World Wide Web, or Internet as we know it today, was something that started with a paper published in 1989, called Information Management: A Proposal. It was intended to find a solution for the sharing of information about the experiments conducted by researchers at CERN, Switzerland.

So the original purpose of the World Wide Web was for some scientists at the CERN labs in Switzerland to share information efficiently about their work. And yet, as you witness every single day and also right now while reading this piece, we have found a myriad of more use cases for the Web Wide Web than just CERN. So much that the World Wide Web is an indispensable part of our everyday lives now.

In the same way, blockchain was invented to enable Bitcoin as an electronic way of payment, but nowadays it’s being used and applied in many other realms. And its application is only ever growing, as we are still realising more and more places where it can be useful.

There is also an ever increasing number of infrastructure and commercial services that have started to appear in order to meet the growing demands of organizations that work with blockchain.

For example, IBM now offers a blockchain platform, as do Amazon and Microsoft. Surely these companies aren’t offering blockchain services and platforms just because of a frenzy, temporary market bubble filled with hype. They’re heavily investing in blockchain technology because they see the demand for it and the future of it. And this demand certainly doesn’t only come from the financial sector.

However, we can all agree that blockchain did not follow a conventional adoption into the business world. The blockchain (and cryptocurrency) has been an unconventional story. Satoshi Nakamoto, who we said initially published the white paper introducing blockchain and Bitcoin, continued to contribute to the original Bitcoin mailing list for a couple of years. But then he went silent, and no one’s been able to find out, myths aside, who he actually is and what happened to him. However, nowadays Satoshi Nakamoto is not really needed for all this to work. The implementation of blockchain is completely public and open source. We will have a look at this implementation and how blockchain works in the next article in this series.

Conclusion

Blockchain was first introduced by Satoshi Nakamoto in a white paper from 2008. It is a technology that works as a digital distributed ledger across a large network of computers.

Historically people have used physical ledgers to keep record of the exchange of goods and services between people. But these ledgers had limitations like being lost, stolen, damaged or maliciously modified. Issues arose especially when ledgers held by different people would not agree and would contain mismatching details for the same transaction. Due to all of these issues, trustworthy, authoritative third parties were introduced. They were often in the form of banks, central banks or other financial institutions. They were tasked with maintaining a single source of truth about transactions and account balances.

But these third parties brought new issues to the picture: delays in transactions, increased costs and privacy issues.

Blockchain as a technology solves all of these shortcomings. As a digital ledger distributed across a vast number of computers worldwide, none of which acts as a single authority, it can keep track in a trustworthy way of all transactions taking place. Due to these amazing qualities, blockchain as a technology has found applications outside of Bitcoin and cryptocurrencies for which it was originally created.

When was blockchain first introduced?

Blockchain was first introduced as a concept in a white paper from Satoshi Nakamoto in 2008. The first blockchain was then built for Bitcoin in 2009.

Is blockchain only used for Bitcoin?

No. Although blockchain was originally developed to support Bitcoin as a cryptocurrency, its advanced technical capabilities make it suitable for a range of other applications.

Is there only one blockchain that exists?

No. Blockchain is a term used to describe the technology. Different blockchains have been developed to date, in order to serve different cryptocurrencies, but also for use cases in industries other than the financial one.

What are some examples of cryptocurrency blockchains?

The Bitcoin blockchain and the Ethereum blockchain are two of the most well known blockchains that exist in the cryptocurrency world. Although the main concept is the same, they each have different implementation details.

$ 117,848.571.77%

$ 3,551.732.26%

$ 3.402.1%

$ 1.000.01%

$ 733.301.26%

$ 176.760.3%

$ 1.000.01%

$ 0.2342827.03%

$ 3,542.612.17%

$ 0.3251472.65%